Get to know how GCOT has been structured organically for the sustainable service model ?

As per the provided provision under Sub-Section 6 of Section 149 of the Companies Act 2013, the following is explanation implies the appointment of Govt. Authorities as Nominee Directors of the GCOT. For ready reference of provision, please see the following;

“Explanation: For the purposes of this section, ―nominee director‖ means a director nominated by any financial institution in pursuance of the provisions of any law for the time being in force, or of any agreement, or appointed by any Government, or any other person to represent its interests.”

Section 161 of Companies Act deals with appointment of additional director, alternate director and nominee director and sub-section (3) of Section 161 says that “Subject to the articles of a company, the Board may appoint any person as a director nominated by any institution in pursuance of the provisions of any law for the time being in force or of any agreement or by the Central Government or the State Government by virtue of its shareholding in a Government company”. As such GCOT while approaching the Govt. Authorities, we shall propose and get the consent from them to appoint as Nominee Director in GCOT.

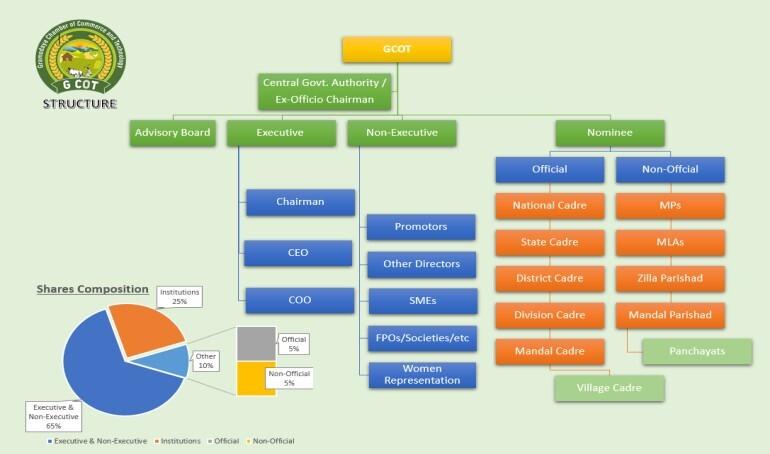

The Board of GCOT is something like General Directorship of Promotors & Members, Official-Directors and Non-Official Directorship. The composition of Board as shown in the above image. According to the Official Cadre, Directorship may be respectively proposed in Agreement / MOU and ascertain their consent along with the Agreement/MOU.

Share holding Pattern:

The Authorised Share Capital of the GCOT is Rs. 10.00 Lakhs with 1.00 Lakh Shares having Rs. 10.00 as share Value. Out of 100% of shareholding, 65% of shares are earmarked for the Individuals and or Institutions, who are actively participant in the GCOT Activities. The remaining 35% shares are earmarked for the individuals and or institutions which don’t take part in activities directly but they shall either provide services to the GCOT or they shall avail the services of the GCOT.

As per the provisions of the section 8 of the Companies act, any category of share holders don't have any right to receive any surplus of the GCOT, as the surplus/profit shall not be distributed to members, but it is used to invest for activities under objectives only.